ATR Trailing Stop Strategy for Protecting Profits

Learn how the ATR Trailing Stop Strategy helps traders lock in profits, reduce emotional exits, and ride strong market trends effectively

Most traders spend months learning how to enter trades.

Very few spend enough time learning how to exit them properly.

That mistake destroys profitability.

A trader can have an excellent entry strategy and still lose money because of poor exit management. Some traders take profits too early out of fear. Others hold winning trades too long and give everything back during reversals.

This is where the ATR Trailing Stop Strategy becomes incredibly powerful.

Instead of guessing where to exit, traders use market volatility to create adaptive stop-loss levels that move with price action. The strategy helps traders protect profits while still giving trades enough room to continue trending.

For algorithmic traders, ATR trailing stops are especially valuable because they can be fully automated using mathematical rules instead of emotional decision-making.

In this guide, you will learn:

- What ATR really measures

- How ATR trailing stops work

- Why volatility-based exits outperform fixed stops

- How to build trend-following systems using ATR

- Risk management techniques for protecting gains

- Python code for ATR trailing stop calculations

- Common mistakes traders make with trailing stops

If you learn how to manage exits intelligently, you may completely transform your long-term trading results.

What Is ATR?

ATR stands for Average True Range.

It is a volatility indicator developed by J. Welles Wilder.

ATR does not predict market direction.

Instead, it measures how much price typically moves over a selected period.

The ATR formula is:

Where:

- ATR represents Average True Range

- n represents the selected lookback period

- TR represents True Range values

True Range is calculated using the largest value among:

- Current high minus current low

- Current high minus previous close

- Current low minus previous close

High ATR values indicate:

- Increased volatility

- Larger price swings

- Faster market movement

Low ATR values indicate:

- Quiet market conditions

- Lower volatility

- Smaller price movement

Why Fixed Stop Losses Often Fail

Many beginner traders use fixed stop losses like:

- 1%

- 2%

- 50 points

- 100 dollars

The problem is that markets are dynamic.

A fixed stop that works during calm conditions may fail completely during volatile periods.

Example:

- Bitcoin can move 500 dollars in minutes during high volatility

- A tiny fixed stop gets hit easily

- The trade later continues in the original direction

ATR solves this problem by adapting stops to current market conditions.

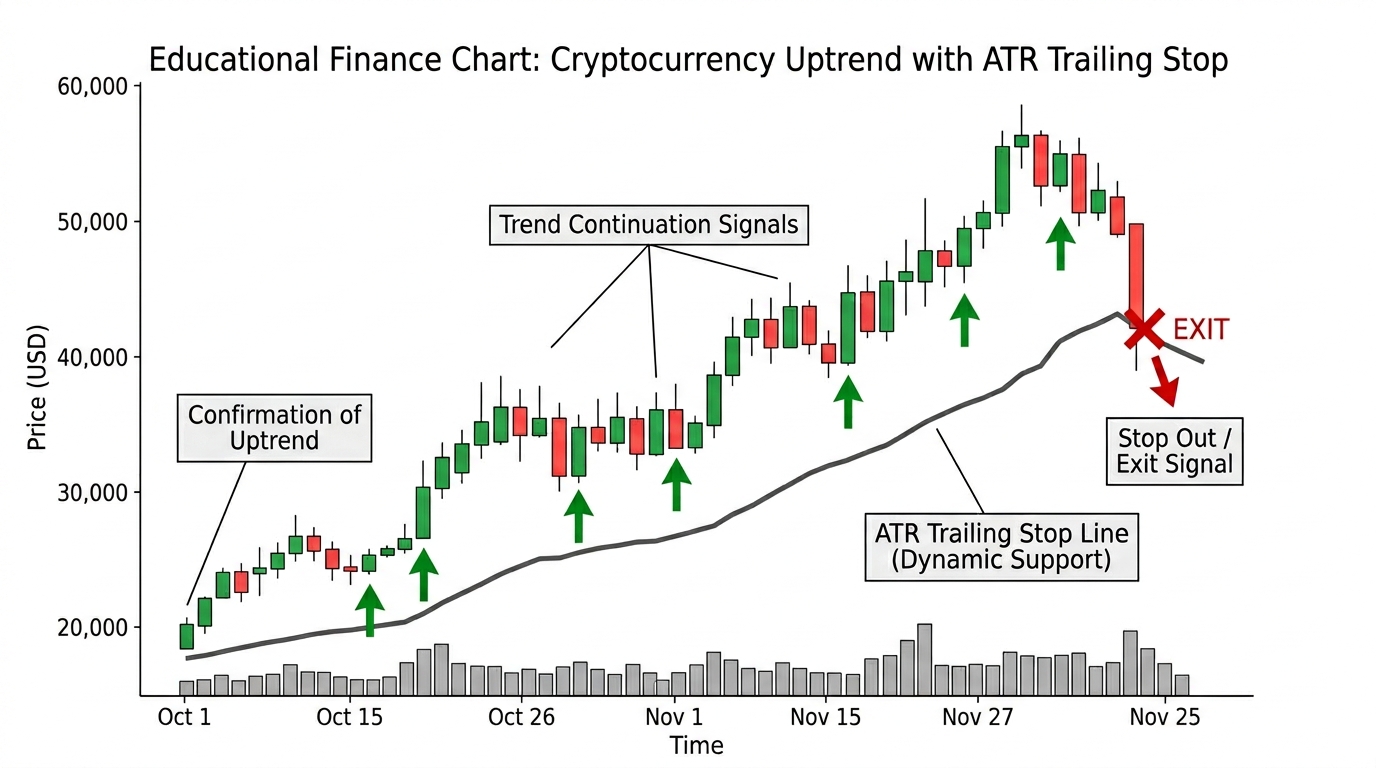

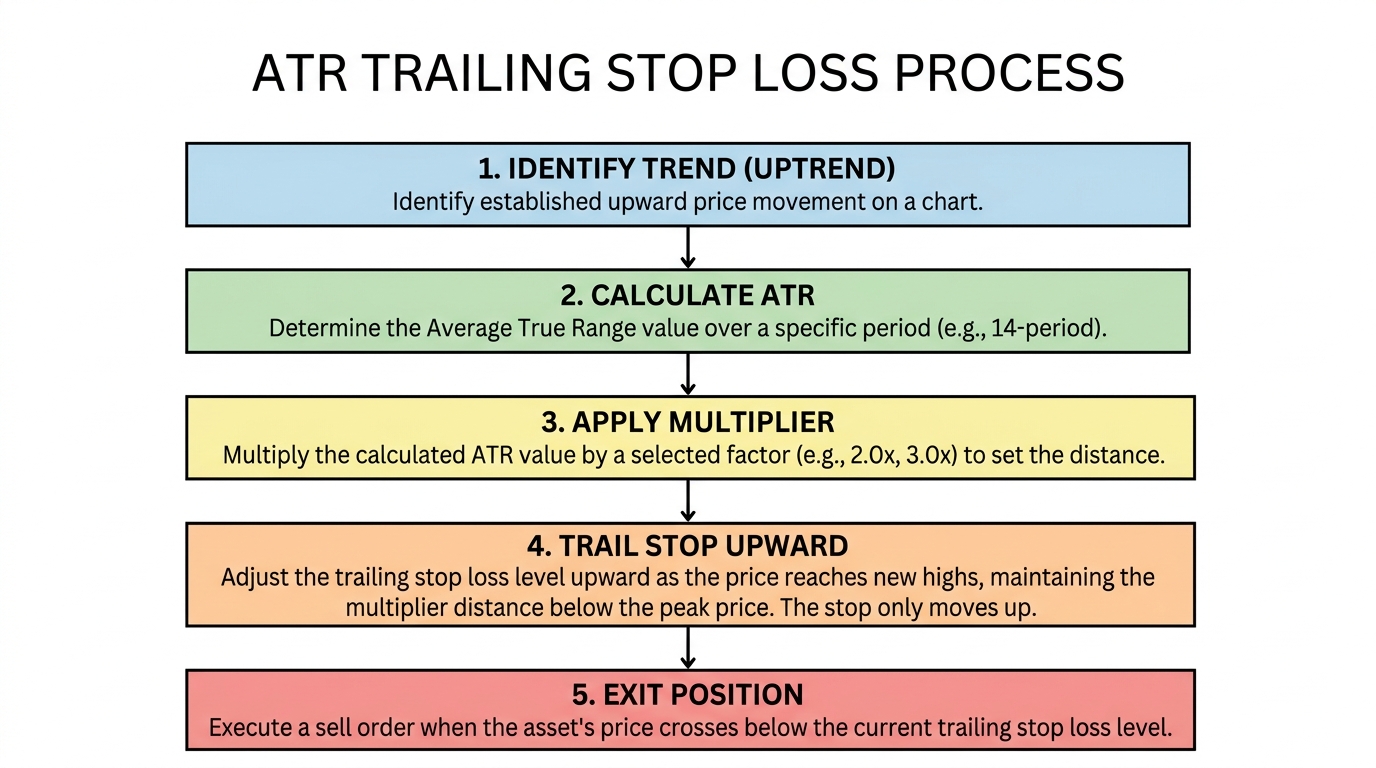

What Is an ATR Trailing Stop?

An ATR trailing stop is a volatility-adjusted stop-loss system.

Instead of placing stops at random distances, traders use ATR multiples to determine stop placement.

As the trade moves in profit:

- The stop moves with price

- The stop locks in gains gradually

- The stop never moves backward

This allows traders to:

- Stay in strong trends longer

- Avoid emotional exits

- Reduce premature stop-outs

- Protect profits systematically

Basic ATR Trailing Stop Formula

A common long-position trailing stop formula is:

Where:

- Highest Price represents the highest price reached during the trade

- ATR represents Average True Range

- k represents the ATR multiplier

Common ATR multipliers include:

- 1.5

- 2

- 3

Larger multipliers:

- Give trades more room

- Reduce stop-outs

- Increase drawdown size

Smaller multipliers:

- Lock profits faster

- Exit trends earlier

- Increase stop sensitivity

Why ATR Trailing Stops Work So Well

Markets rarely move in straight lines.

Even strong trends experience:

- Pullbacks

- Consolidations

- Temporary volatility spikes

A trailing stop based on ATR adapts naturally to these fluctuations.

This creates a balance between:

- Protecting profits

- Allowing trend continuation

That balance is critical in crypto trading where volatility is extreme.

Example of an ATR Trailing Stop

Imagine:

- Bitcoin trades at 60,000

- ATR equals 800

- ATR multiplier equals 2

The trailing stop distance becomes:

Plain text example:

800 multiplied by 2 equals 1,600.

If the highest price during the trade becomes 63,000:

Plain text example:

63,000 minus 1,600 equals 61,400.

The stop would move upward as price rises.

If price later falls to 61,400, the trade exits automatically.

Why Crypto Traders Love ATR Stops

Crypto markets are highly volatile.

Fixed stops often fail because:

- Volatility changes rapidly

- News events trigger sharp spikes

- Liquidation cascades create noise

ATR trailing stops adjust dynamically to:

- Market speed

- Volatility expansion

- Trend strength

This makes them ideal for:

- Bitcoin trend following

- Altcoin momentum trading

- Swing trading

- Breakout systems

ATR Trailing Stops for Trend Following

Trend traders often face one major problem:

“How do I stay in the trend long enough?”

Most traders exit too early.

ATR trailing stops help traders remain in strong trends without guessing exit points.

The strategy works especially well during:

- Bull markets

- Momentum breakouts

- Strong directional trends

Best ATR Multipliers for Different Trading Styles

Different strategies require different stop sensitivity.

Scalping

- ATR multiplier between 1 and 1.5

Day Trading

- ATR multiplier between 1.5 and 2

Swing Trading

- ATR multiplier between 2 and 3

Position Trading

- ATR multiplier between 3 and 5

There is no universal perfect setting.

Backtesting is essential.

Combining ATR Stops With Market Structure

Professional traders rarely rely on ATR alone.

ATR works better when combined with:

- Support and resistance

- Swing highs and lows

- Trend analysis

- Volume confirmation

Example:

- Place ATR stop below key support

- Align stop with market structure

This reduces weak exits caused by random volatility.

ATR Position Sizing Strategy

ATR can also improve position sizing.

The position sizing formula is:

Where:

- Position Size determines trade exposure

- Risk Per Trade represents acceptable loss amount

- ATR measures market volatility

- k represents the ATR multiplier

Plain text example:

If risking 100 dollars with an ATR stop distance of 200 dollars, the position size would equal 0.5 units.

This keeps risk consistent even when volatility changes.

ATR Trailing Stops During Volatility Expansion

One fascinating feature of ATR is that it expands during chaotic conditions.

That means:

- Stops automatically widen during volatility spikes

- Stops tighten during calm markets

This dynamic adjustment helps traders survive temporary market noise.

Python Code for ATR Trailing Stop Strategy

Here is a simple Python example for calculating ATR trailing stops.

1import pandas as pd

2import numpy as np

3

4# Calculate True Range

5df['H-L'] = df['high'] - df['low']

6df['H-PC'] = abs(df['high'] - df['close'].shift(1))

7df['L-PC'] = abs(df['low'] - df['close'].shift(1))

8

9df['TR'] = df[['H-L', 'H-PC', 'L-PC']].max(axis=1)

10

11# Calculate ATR

12df['ATR'] = df['TR'].rolling(14).mean()

13

14# ATR multiplier

15multiplier = 2

16

17# Trailing stop calculation

18df['Trailing_Stop'] = (

19df['close'].rolling(1).max() - (df['ATR'] * multiplier)

20)This script:

- Calculates True Range

- Computes ATR values

- Builds a simple trailing stop model

Advanced traders often improve this by adding:

- Trend filters

- Volume conditions

- Multi-timeframe confirmation

- Dynamic multipliers

ATR Trailing Stop vs Fixed Take Profit

Many beginners use fixed targets like:

- 2%

- 5%

- 10%

The problem is that trends sometimes continue much further.

ATR trailing stops allow traders to:

- Capture larger moves

- Let winners run

- Exit naturally when momentum weakens

This often improves long-term profitability.

Common ATR Trailing Stop Mistakes

Using Extremely Tight Multipliers

Small ATR multipliers create excessive stop-outs.

The trade never gets enough breathing room.

Ignoring Market Conditions

Volatile markets need wider stops.

Calm markets may allow tighter trailing behavior.

Moving Stops Emotionally

Some traders manually override trailing stops because of fear.

This destroys system consistency.

Using ATR Without Trend Analysis

ATR measures volatility, not direction.

Always combine ATR with trend confirmation.

Forgetting Backtesting

Every market behaves differently.

Bitcoin volatility differs from forex volatility. Altcoins behave differently from large-cap assets.

Test your settings carefully.

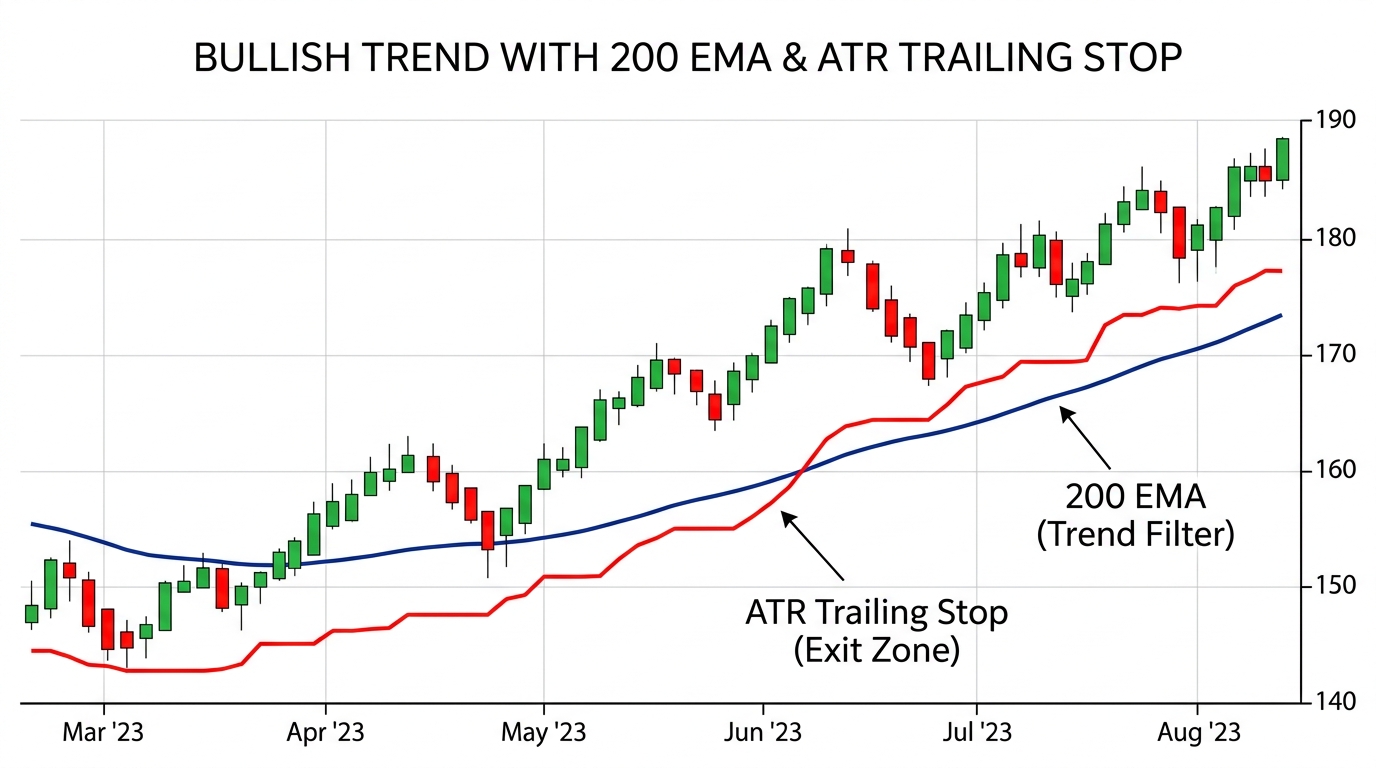

ATR Trailing Stops With Moving Averages

A powerful combination is:

- ATR trailing stop

- Long-term moving average filter

Example:

- Only take long trades above the 200 EMA

- Use ATR trailing stop for exits

This keeps traders aligned with major trends.

Multi-Timeframe ATR Strategy

Advanced traders often combine ATR signals across multiple timeframes.

Example:

- Daily chart defines main trend

- 1-hour chart handles trade execution

- ATR stop adapts to lower timeframe volatility

This creates more precise entries and exits.

Using ATR Stops in Automated Trading Systems

Algo traders prefer ATR because it is:

- Quantifiable

- Adaptive

- Easy to code

- Highly flexible

ATR trailing stops work well in:

- Trend-following bots

- Breakout systems

- Momentum strategies

- Swing trading automation

Because the rules are objective, traders reduce emotional decision-making dramatically.

Key Takeaways

- ATR measures market volatility

- ATR trailing stops adapt to changing conditions

- Volatility-based exits outperform many fixed stops

- ATR helps traders stay in trends longer

- Combining ATR with structure improves reliability

- Risk management becomes more systematic

- Python makes ATR automation straightforward

Conclusion

The ATR Trailing Stop Strategy solves one of the hardest problems in trading:

Knowing when to exit.

Most traders obsess over entries while completely ignoring trade management. But in reality, intelligent exits often separate profitable traders from losing traders.

ATR trailing stops create structure during uncertainty.

Instead of emotionally guessing:

- When to take profit

- When to hold longer

- When to exit losing momentum

…traders use volatility itself as the decision-making framework.

That changes everything.

When combined with:

- Trend analysis

- Risk management

- Position sizing

- Systematic execution

- Backtesting

the ATR trailing stop becomes a professional-grade tool for protecting profits while maximizing trend opportunities.

Start simple.

Open historical charts. Plot ATR trailing stops manually. Observe how trends behave around them. Then automate the strategy with Python.

Over time, you may discover that smarter exits can improve your trading performance more than finding new entries ever could.