AI Trading Systems That Adapt to Market Conditions

Learn how adaptive AI trading systems use Hidden Markov Models for regime detection, online learning for continuous adaptation, reinforcement learning for policy optimization, and adaptive ensemble weighting to stay profitable as market conditions shift — with complete Python implementation.

Introduction: The Strategy That Worked Last Year Is Already Obsolete

In 2021, a simple momentum strategy applied to crypto would have made you look like a genius. Buy what was going up; it kept going up. Trend-following systems posted extraordinary returns. Volatility was high but directional. The market rewarded aggression.

In 2022, that same strategy would have destroyed your account. The macro regime shifted — rising interest rates, collapsing liquidity, risk-off sentiment across all asset classes — and momentum signals that had been reliably profitable inverted. Traders who had not adapted lost not just their 2022 gains but much of what they had earned in 2021.

This is the central problem of algorithmic trading that almost no beginner-to-intermediate resource addresses directly: a strategy that is not designed to adapt is not a strategy — it is a bet on regime persistence. And regimes, by definition, end.

The solution is not to build a better static model. It is to build systems that detect when market conditions change and respond accordingly — systems that carry different playbooks for trending markets, ranging markets, high-volatility regimes, and low-volatility environments, and route signals through the appropriate playbook based on current conditions.

In this post, you will learn exactly how to build adaptive AI trading systems. You will understand Hidden Markov Model-based regime detection, online learning that updates model parameters in real time, ensemble architectures that weight different strategies by regime, and the foundations of reinforcement learning for trading. Code is included throughout.

The Anatomy of a Static System's Failure

Before building adaptive systems, it is worth being precise about why static systems fail. The failure mode is elegant in its predictability.

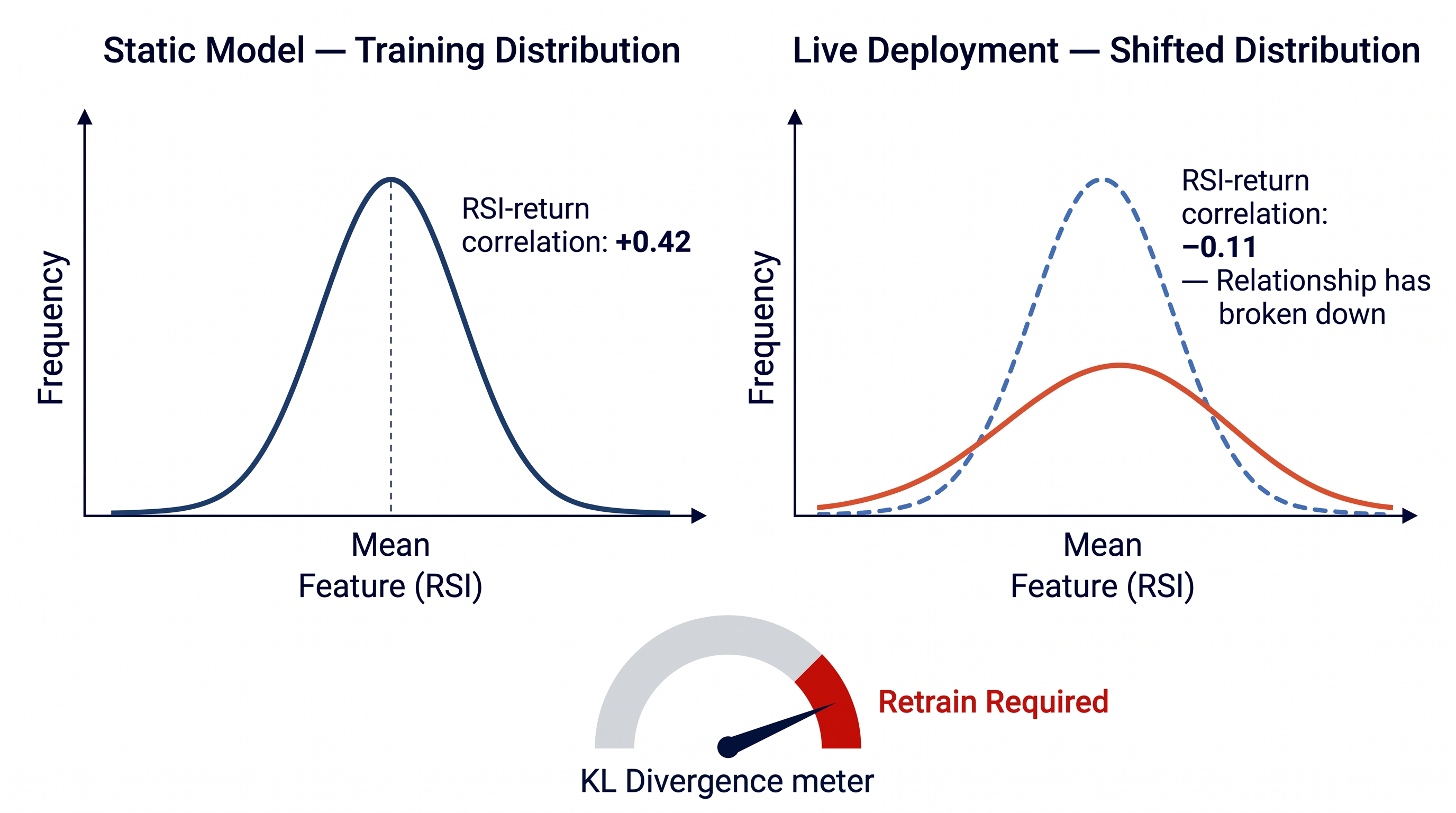

Every machine learning model trained on historical data implicitly assumes that the statistical relationships it learned will persist into the future. A Random Forest trained on 2019–2021 data learns that RSI below 30 combined with high volume tends to precede upward moves. That relationship held in a particular macro environment — one characterized by zero interest rates, institutional FOMO, and retail speculation. When that environment ended, the relationship weakened, then inverted in some regimes entirely.

The formal description of this problem is distribution shift — the training distribution diverges from the deployment distribution . A static model has no mechanism for detecting or responding to this divergence.

The Kullback-Leibler divergence measures the distance between two distributions:

When between your training distribution and the current market distribution exceeds a meaningful threshold, your model's predictions are based on relationships that no longer hold. An adaptive system monitors this divergence and triggers retraining or regime switching when it exceeds a threshold.

Regime Detection: Teaching Your System to Read the Market

The first layer of any adaptive trading system is regime detection — a model or rule set that classifies the current market state into one of several distinct regimes, each associated with different expected asset behavior.

Four regimes cover the majority of market environments: trending up, trending down, ranging (low directional conviction), and high-volatility crisis. Each regime has a distinct signal-generating strategy that performs best within it.

Rule-Based Regime Detection

The simplest approach uses observable market indicators — ADX for trend strength, realized volatility for regime type, and EMA slope for direction:

1import pandas as pd

2import numpy as np

3

4def detect_regime_rules(df, adx_threshold=25, vol_lookback=20,

5 ema_period=200, vol_multiplier=1.5):

6 """Rule-based market regime detection using ADX, volatility, and EMA slope."""

7 close = df['close']

8

9 ema200 = close.ewm(span=ema_period, adjust=False).mean()

10 ema_slope = ema200.diff(5) / ema200.shift(5)

11

12 log_ret = np.log(close / close.shift(1))

13 vol = log_ret.rolling(vol_lookback).std() * np.sqrt(365)

14 vol_long = log_ret.rolling(vol_lookback * 3).std() * np.sqrt(365)

15

16 vol_ratio = vol / vol_long

17

18 regimes = []

19 for i in range(len(df)):

20 current_vol_ratio = vol_ratio.iloc[i] if i < len(vol_ratio) else np.nan

21 current_slope = ema_slope.iloc[i] if i < len(ema_slope) else np.nan

22 current_vol = vol.iloc[i] if i < len(vol) else np.nan

23 long_vol = vol_long.iloc[i] if i < len(vol_long) else np.nan

24

25 if pd.isna(current_vol_ratio) or pd.isna(current_slope):

26 regimes.append('unknown')

27 elif current_vol > long_vol * vol_multiplier:

28 regimes.append('crisis')

29 elif current_vol_ratio > 1.2 and current_slope > 0:

30 regimes.append('uptrend')

31 elif current_vol_ratio > 1.2 and current_slope < 0:

32 regimes.append('downtrend')

33 else:

34 regimes.append('ranging')

35

36 df['regime'] = regimes

37 return dfHidden Markov Models for Statistical Regime Detection

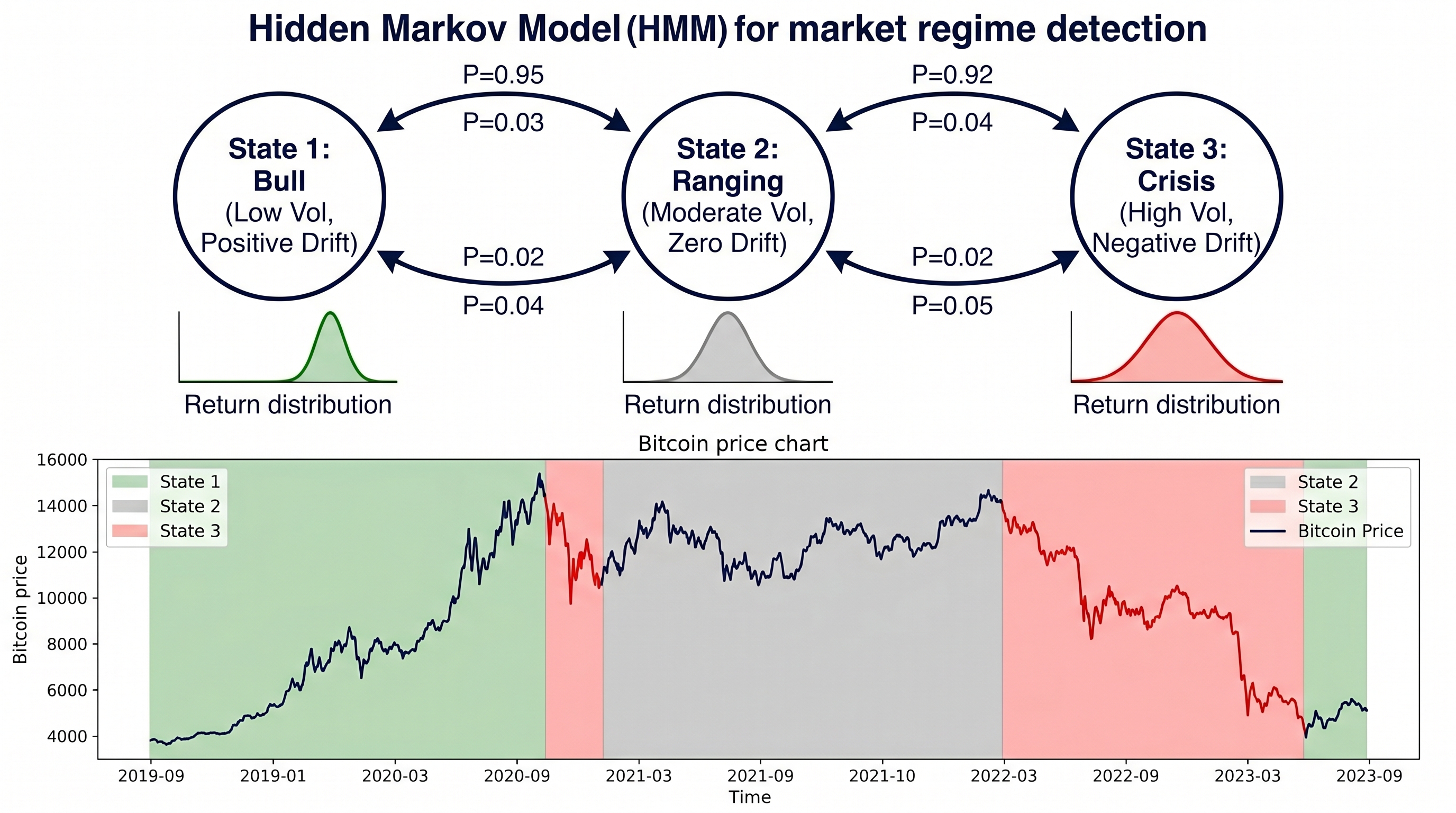

A Hidden Markov Model (HMM) assumes the market is always in one of hidden states, each generating observable returns with state-specific statistical properties. The likelihood of observing return given state :

Where and are the mean return and volatility of state . The model also learns a transition matrix where , encoding the probability of transitioning from regime to .

1from hmmlearn import hmm

2

3def fit_hmm_regime_model(returns, n_states=3):

4 """Fit a Gaussian HMM to return series and detect market regimes."""

5 obs = returns.dropna().values.reshape(-1, 1)

6

7 model = hmm.GaussianHMM(

8 n_components=n_states,

9 covariance_type='full',

10 n_iter=1000,

11 random_state=42

12 )

13 model.fit(obs)

14

15 hidden_states = model.predict(obs)

16

17 state_stats = {}

18 for state in range(n_states):

19 mask = hidden_states == state

20 state_returns = obs[mask]

21 state_stats[state] = {

22 'mean_return': np.mean(state_returns),

23 'volatility': np.std(state_returns),

24 'frequency': np.mean(mask)

25 }

26 print(f"State {state}: Mean={np.mean(state_returns):.5f}, "

27 f"Vol={np.std(state_returns):.5f}, Freq={np.mean(mask):.3f}")

28

29 return model, hidden_states, state_statsThe three states a Gaussian HMM typically discovers in crypto data correspond to: a low-volatility, positive-drift bull state; a moderate-volatility, near-zero-drift ranging state; and a high-volatility, negative-drift crisis state.

Regime-Conditional Strategy Routing: The Signal Switching Architecture

1class RegimeConditionalTrader:

2 """Adaptive trading system routing signals through regime-specific models."""

3

4 def __init__(self):

5 self.regime_models = {}

6 self.current_regime = None

7

8 def register_strategy(self, regime_name, model, signal_generator):

9 self.regime_models[regime_name] = {

10 'model': model, 'signal_fn': signal_generator

11 }

12

13 def detect_regime(self, features, hmm_model):

14 obs = features['log_return'].values[-20:].reshape(-1, 1)

15 state = hmm_model.predict(obs)[-1]

16 state_to_regime = {0: 'bull', 1: 'ranging', 2: 'crisis'}

17 self.current_regime = state_to_regime.get(state, 'ranging')

18 return self.current_regime

19

20 def generate_signal(self, features):

21 if self.current_regime not in self.regime_models:

22 return 0

23 strategy = self.regime_models[self.current_regime]

24 return strategy['signal_fn'](features, strategy['model'])Each regime-specific model is trained exclusively on data labeled as that regime — the bull market model has never seen bear market data and has not learned spurious patterns from the wrong environment.

Online Learning: Real-Time Model Adaptation

Regime switching handles discrete shifts. But markets also drift continuously. Online learning — updating model parameters as new data arrives — addresses this using exponentially weighted updates:

Smaller weights history more heavily producing more stable estimates. Larger adapts faster but produces noisier estimates.

1from sklearn.linear_model import SGDClassifier

2import numpy as np

3

4class OnlineLearningTrader:

5 """Trading model updating incrementally via stochastic gradient descent."""

6

7 def __init__(self, learning_rate=0.01, regularization=0.001):

8 self.model = SGDClassifier(

9 loss='log_loss',

10 learning_rate='constant',

11 eta0=learning_rate,

12 alpha=regularization,

13 warm_start=True # Preserve weights between partial_fit calls

14 )

15 self.classes = np.array([-1, 0, 1])

16 self.is_initialized = False

17 self.update_count = 0

18

19 def partial_fit(self, X_seed, y_seed):

20 """Initialize model with seed data."""

21 self.model.partial_fit(X_seed, y_seed, classes=self.classes)

22 self.is_initialized = True

23

24 def predict(self, X):

25 """Generate signal with confidence."""

26 if not self.is_initialized:

27 return 0, 0.333

28 proba = self.model.predict_proba(X.reshape(1, -1))[0]

29 class_idx = np.argmax(proba)

30 return self.classes[class_idx], proba[class_idx]

31

32 def update(self, X, y_true):

33 """Update model with new observation."""

34 self.model.partial_fit(X.reshape(1, -1), [y_true])

35 self.update_count += 1The tension is between stability and plasticity. A model adapting too quickly forgets valid patterns; one adapting too slowly fails to capture regime changes. The optimal learning rate can be coupled to the detected regime volatility.

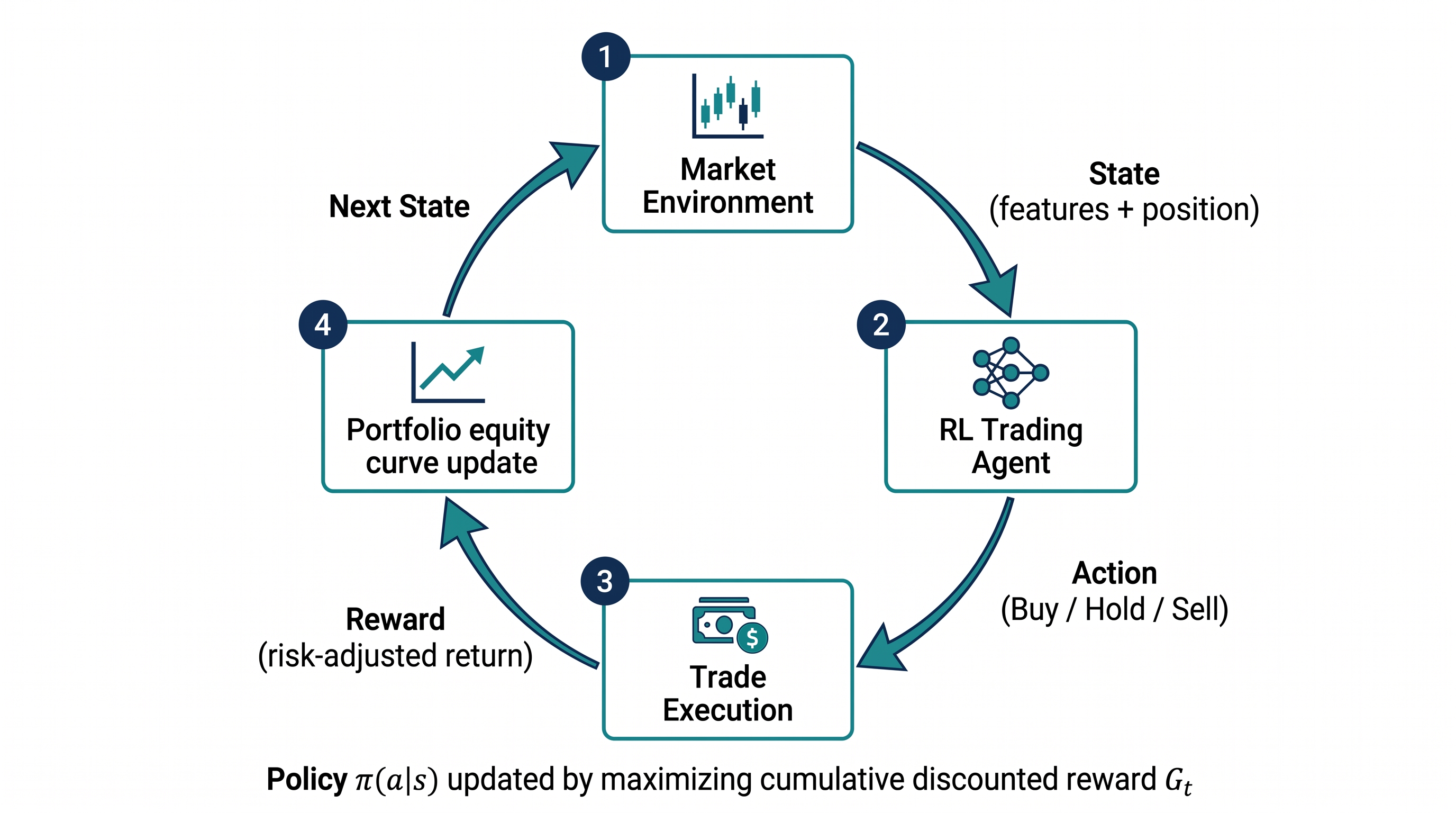

Reinforcement Learning: The Self-Improving Trader

RL treats trading as a sequential decision problem. The agent's objective is to maximize cumulative discounted reward:

Where is the discount factor — close to 1 means long-term planning, close to 0 means myopic optimization.

1class TradingEnvironment:

2 """Reinforcement learning environment for crypto trading."""

3

4 def __init__(self, price_series, features_df, initial_capital=10000,

5 transaction_cost=0.001, window=20):

6 self.prices = price_series.values

7 self.features = features_df.values

8 self.capital = initial_capital

9 self.initial_capital = initial_capital

10 self.tc = transaction_cost

11 self.window = window

12 self.reset()

13

14 def reset(self):

15 self.t = self.window

16 self.position = 0 # -1 short, 0 flat, 1 long

17 self.capital = self.initial_capital

18 self.portfolio_value = self.initial_capital

19 self.done = False

20 return self._get_state()

21

22 def _get_state(self):

23 market_state = self.features[self.t - self.window:self.t].flatten()

24 position_state = np.array([self.position])

25 return np.concatenate([market_state, position_state])

26

27 def step(self, action):

28 """Actions: 0=Sell/Short, 1=Hold, 2=Buy/Long"""

29 new_position = action - 1 # {0,1,2} → {-1,0,1}

30 price_return = (self.prices[self.t] - self.prices[self.t - 1]) / self.prices[self.t - 1]

31 position_return = self.position * price_return

32

33 if new_position != self.position:

34 position_return -= self.tc

35

36 self.portfolio_value *= (1 + position_return)

37 self.position = new_position

38 reward = position_return

39 self.t += 1

40 self.done = self.t >= len(self.prices) - 1

41 return self._get_state() if not self.done else None, reward, self.doneA risk-adjusted reward function teaches the agent to balance return against drawdown:

This tells the agent that a 2% return with low volatility is more valuable than a 2% return with high volatility.

The Adaptive Ensemble: Combining Multiple Strategies by Regime Weight

The most robust adaptive systems blend strategies rather than switching entirely:

Weights are updated using an exponentially weighted average of recent performance:

1class AdaptiveEnsemble:

2 """Ensemble dynamically weighting strategy signals by rolling Sharpe."""

3

4 def __init__(self, strategy_names, lookback=60, temperature=2.0):

5 self.strategy_names = strategy_names

6 self.lookback = lookback

7 self.temperature = temperature

8 self.return_histories = {name: [] for name in strategy_names}

9

10 def compute_weights(self):

11 sharpe_estimates = {}

12 for name in self.strategy_names:

13 hist = self.return_histories[name][-self.lookback:]

14 if len(hist) < 10:

15 sharpe_estimates[name] = 0.0

16 else:

17 mean_ret, std_ret = np.mean(hist), np.std(hist)

18 sharpe_estimates[name] = mean_ret / std_ret if std_ret > 0 else 0.0

19

20 sharpe_array = np.array(list(sharpe_estimates.values()))

21 exp_sharpe = np.exp(self.temperature * sharpe_array)

22 weights = exp_sharpe / exp_sharpe.sum()

23 return dict(zip(self.strategy_names, weights))

24

25 def blend_signals(self, signals_dict):

26 weights = self.compute_weights()

27 blended = sum(weights[name] * signal for name, signal in signals_dict.items())

28 return blended, weightsThis ensemble is self-correcting: as a strategy degrades in the current regime, its rolling Sharpe falls, its weight decreases, and the system naturally de-emphasizes its signal. When conditions shift to favor it again, its weight recovers automatically.

Performance Monitoring and Automatic Retraining

The Page-Cusum test detects structural breaks in model performance:

When exceeds threshold , a structural break is flagged and retraining is triggered:

1def cusum_monitor(returns, mu_0=0.0001, k=0.0002, h=0.005):

2 """CUSUM test for detecting performance degradation."""

3 C = 0.0

4 alerts = []

5 for ret in returns:

6 C = max(0, C + (ret - mu_0) - k)

7 if C > h:

8 alerts.append(True)

9 C = 0.0 # Reset after alert

10 else:

11 alerts.append(False)

12 return alertsKey Takeaways

- Static trading models are bets on regime persistence — they fail when market conditions shift, which they inevitably do

- Hidden Markov Models are the most principled approach to regime detection — learning hidden states and transition probabilities directly from return data

- Regime-conditional signal routing assigns different strategy models to different environments, ensuring each operates within its trained conditions

- Online learning via stochastic gradient descent updates parameters continuously, addressing gradual drift within regimes

- Reinforcement learning treats trading as sequential decision-making with explicit reward feedback, discovering policies not pre-specified by the designer

- Adaptive ensemble weighting using softmax over rolling Sharpe ratios creates a self-correcting system that automatically concentrates on best-performing strategies

- Performance monitoring with CUSUM tests provides statistical detection of degradation and triggers retraining before losses accumulate

Conclusion: Adaptability Is the Only Durable Edge

The markets of 2026 are different from the markets of 2021. The markets of 2028 will be different again. New participants enter, old participants adapt, liquidity conditions shift, macro regimes rotate, and the statistical relationships that powered last year's edge decay as more capital discovers and arbitrages them away.

In this environment, the only genuinely durable edge is architectural: a system designed to detect change, adapt its behavior, and maintain its edge across the full cycle of market regimes.

The building blocks are all accessible to a Python-familiar algorithmic trader today. Hidden Markov Models in hmmlearn. Online learning via scikit-learn's partial_fit. Simple RL environments using the patterns above, extendable to stable-baselines3. Adaptive ensemble weighting with NumPy arithmetic.

Start with regime detection. Apply a three-state Gaussian HMM to two years of daily returns for your primary trading asset. Visualize the detected regimes against price history. Build one regime-specific strategy for your most clearly defined regime: the crisis state, where behavior is most distinctive.

From there, the system grows one component at a time — in the patient, deliberate layering of components that each solve a specific failure mode of the static approach.

The market rewards adaptation. Build systems that adapt.