AI Trading System Architecture Explained

Learn how to architect a complete AI trading system end-to-end — seven production layers from data ingestion and feature engineering through model inference, signal generation, risk management, order execution, and monitoring. Full Python implementation with Kelly sizing and rolling AUC circuit breakers.

Introduction: The Model Is the Easy Part

Most algo traders who get serious about AI-powered trading spend the majority of their time on the model. They obsess over architecture choices — LSTM versus transformer, Random Forest versus XGBoost, tune hyperparameters for weeks, and celebrate when validation AUC ticks above 0.57. Then they try to deploy, and the system falls apart within days.

The data feed disconnects silently. The order sizing logic sends a position ten times larger than intended. The model retrains on stale data. The execution layer ignores slippage. The monitoring dashboard shows everything green while the account bleeds.

Here is the counterintuitive insight that professional quant developers learn, usually painfully: the model is the easy part. Any competent Python developer can train a gradient-boosted classifier on OHLCV features in an afternoon. Building the system that keeps that model running reliably — ingesting clean data, generating signals consistently, executing trades safely, monitoring performance honestly, and retraining intelligently — is the genuinely hard work. And it is the work almost nobody teaches.

In this post, you will learn the complete architecture of a production-grade AI trading system, layer by layer. You will understand what belongs in each component, how components communicate, where systems most commonly fail, and how to implement each layer in Python.

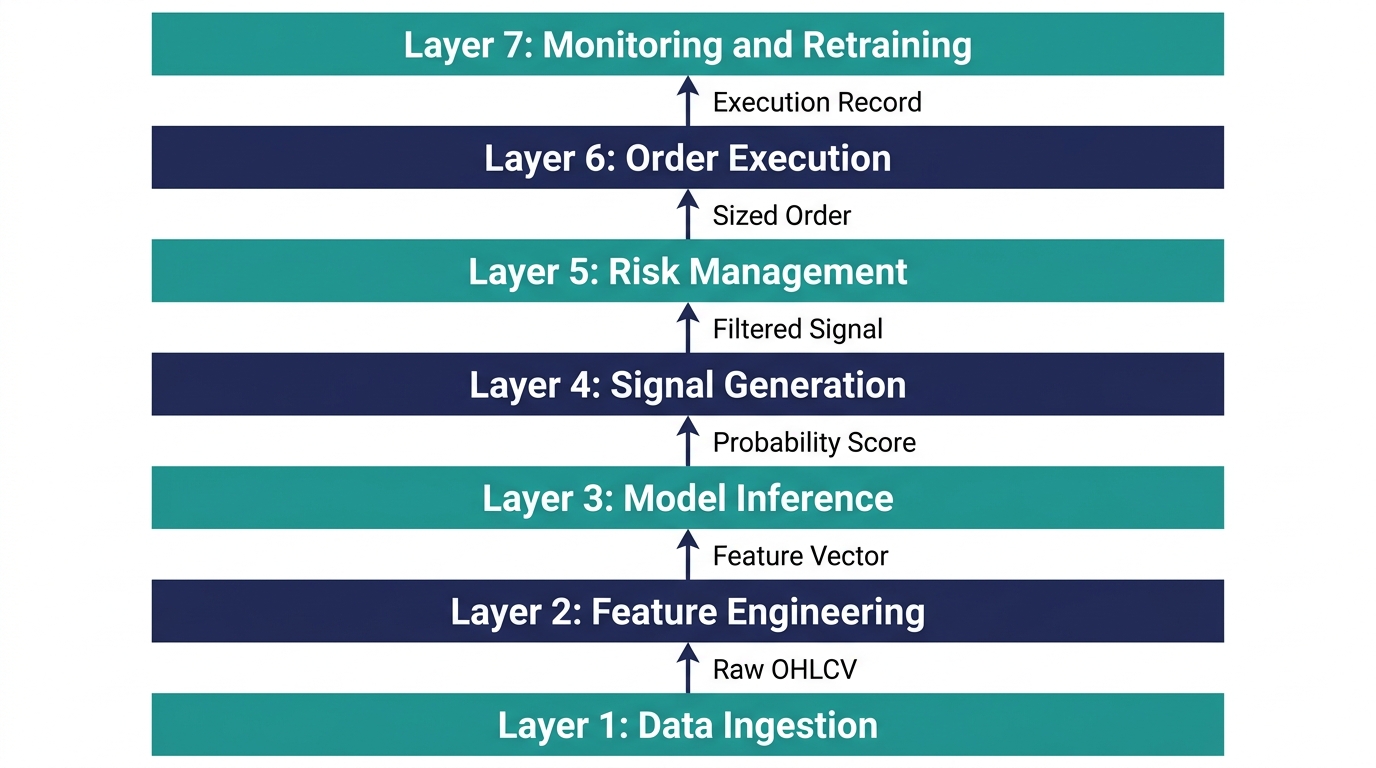

The Seven Layers of a Production AI Trading System

A well-architected AI trading system is not a single script — it is a pipeline of distinct, independently maintainable components, each with a clearly defined responsibility. When systems fail, the failure is almost always in one of these layers, or in the interfaces between them.

The seven layers are: data ingestion, feature engineering, model inference, signal generation, risk management, order execution, and monitoring and retraining. Each operates independently. Each has defined inputs and outputs. Each can fail independently, and each should be monitored independently.

Layer 1: Data Ingestion — The Foundation That Everything Rests On

If your data pipeline is unreliable, everything built on top of it is unreliable. This layer acquires, validates, stores, and serves market data continuously, without silent failures, under real-world network conditions.

A production data ingestion layer handles two fundamentally different data modes simultaneously. Historical data for training is acquired in batch from exchange APIs. Real-time data for live inference arrives continuously via WebSocket streams. The critical design principle: historical and real-time data must pass through identical normalization and validation logic. This is what makes backtests meaningful.

1import ccxt

2import pandas as pd

3import time

4import logging

5from datetime import datetime, timezone

6

7logging.basicConfig(level=logging.INFO, format='%(asctime)s %(levelname)s %(message)s')

8

9class DataIngestionLayer:

10 """Handles historical OHLCV fetch and basic data validation."""

11

12 def __init__(self, exchange_id='binance', symbol='BTC/USDT', timeframe='1d'):

13 self.exchange = getattr(ccxt, exchange_id)({'enableRateLimit': True})

14 self.symbol = symbol

15 self.timeframe = timeframe

16

17 def fetch_ohlcv(self, since_days=365):

18 """Fetch historical OHLCV with automatic pagination and validation."""

19 since_ms = int((datetime.now(timezone.utc).timestamp() - since_days * 86400) * 1000)

20 all_candles = []

21

22 logging.info(f"Fetching {self.symbol} {self.timeframe} data from {self.exchange.id}")

23

24 while True:

25 candles = self.exchange.fetch_ohlcv(self.symbol, self.timeframe, since=since_ms, limit=500)

26 if not candles:

27 break

28 all_candles.extend(candles)

29 since_ms = candles[-1][0] + 1

30 time.sleep(self.exchange.rateLimit / 1000)

31 if len(candles) < 500:

32 break

33

34 df = pd.DataFrame(all_candles, columns=['timestamp', 'open', 'high', 'low', 'close', 'volume'])

35 df['timestamp'] = pd.to_datetime(df['timestamp'], unit='ms', utc=True)

36 df.set_index('timestamp', inplace=True)

37 return self._validate(df)

38

39 def _validate(self, df):

40 """Data quality validation — fail loudly on bad data."""

41 initial_len = len(df)

42 df = df[~df.index.duplicated(keep='last')]

43 df = df[(df[['open', 'high', 'low', 'close']] > 0).all(axis=1)]

44 df = df[df['high'] >= df['low']]

45 df = df[df['volume'] > 0]

46

47 removed = initial_len - len(df)

48 if removed > 0:

49 logging.warning(f"Validation removed {removed} malformed rows ({100*removed/initial_len:.1f}%)")

50 return df.sort_index()The _validate method is not optional. In production, exchange APIs regularly return malformed candles, zero-volume rows during outages, duplicate timestamps from API glitches, and candles where high is less than low. Downstream components that receive malformed data will produce NaN or infinite feature values that propagate silently and corrupt model inference.

Layer 2: Feature Engineering — Where Raw Data Becomes Predictive Information

Feature engineering is the translation layer between raw market data and numerical model inputs. In a well-architected system, all feature computation lives in a single, version-controlled module called identically in training, backtesting, and live inference. Separate feature code for training and live inference guarantees silent performance degradation.

1class FeatureEngineeringLayer:

2 """Computes all model features from validated OHLCV data. Single source of truth."""

3

4 def compute_features(self, df: pd.DataFrame) -> pd.DataFrame:

5 features = df.copy()

6 features['log_return'] = np.log(features['close'] / features['close'].shift(1))

7

8 delta = features['close'].diff()

9 gain = delta.clip(lower=0).rolling(14).mean()

10 loss = -delta.clip(upper=0).rolling(14).mean()

11 features['rsi'] = 100 - (100 / (1 + gain / loss))

12

13 sma20 = features['close'].rolling(20).mean()

14 std20 = features['close'].rolling(20).std()

15 features['bb_width'] = (2 * std20) / sma20

16

17 features['volatility'] = features['log_return'].rolling(10).std() * np.sqrt(252)

18

19 vol_mean = features['volume'].rolling(20).mean()

20 vol_std = features['volume'].rolling(20).std()

21 features['vol_zscore'] = (features['volume'] - vol_mean) / vol_std

22

23 for lag in [1, 2, 3, 5, 10]:

24 features[f'lag_{lag}'] = features['log_return'].shift(lag)

25

26 features.dropna(inplace=True)

27 return features

28

29 def get_feature_columns(self):

30 return ['rsi', 'bb_width', 'volatility', 'vol_zscore',

31 'lag_1', 'lag_2', 'lag_3', 'lag_5', 'lag_10']The Bollinger Band width: . Annualized rolling volatility: . Both formulas use only past data at each time step — no centered windows, no future-referencing calculations. This is enforced by the architecture, not left to individual developer discipline.

Layer 3: Model Inference — Turning Features Into Probabilities

The model inference layer receives a feature vector and returns a probability estimate. It knows nothing about data sources, trading logic, or execution — it simply wraps a trained model and exposes a predict interface.

1import joblib

2

3class ModelInferenceLayer:

4 """Wraps a trained model and scaler for live inference."""

5

6 def __init__(self, model_path='model.joblib', scaler_path='scaler.joblib'):

7 self.model = joblib.load(model_path)

8 self.scaler = joblib.load(scaler_path)

9

10 def predict(self, feature_vector: np.ndarray) -> dict:

11 scaled = self.scaler.transform(feature_vector.reshape(1, -1))

12 prob_up = self.model.predict_proba(scaled)[0, 1]

13

14 return {

15 'probability_up': round(float(prob_up), 4),

16 'probability_down': round(float(1 - prob_up), 4),

17 'confidence': round(float(abs(prob_up - 0.5) * 2), 4),

18 'raw_prediction': int(prob_up > 0.5)

19 }

20

21 @classmethod

22 def train_and_save(cls, X_train, y_train, feature_cols,

23 model_path='model.joblib', scaler_path='scaler.joblib'):

24 scaler = StandardScaler()

25 X_scaled = scaler.fit_transform(X_train)

26 model = RandomForestClassifier(

27 n_estimators=300, max_depth=6, min_samples_leaf=20,

28 class_weight='balanced', random_state=42, n_jobs=-1

29 )

30 model.fit(X_scaled, y_train)

31 joblib.dump(model, model_path)

32 joblib.dump(scaler, scaler_path)

33 return cls(model_path, scaler_path)The confidence score transforms raw probability into a 0-to-1 scale where 0 means complete uncertainty and 1 means complete certainty: .

Layer 4: Signal Generation — From Probability to Trading Decision

The signal generation layer applies filtering logic — confidence thresholding, signal deduplication, and optionally regime filtering.

1from dataclasses import dataclass

2from typing import Optional

3from datetime import datetime

4

5@dataclass

6class TradingSignal:

7 timestamp: datetime

8 direction: str # 'long', 'short', or 'flat'

9 confidence: float

10 probability_up: float

11 source_model: str

12 regime: Optional[str] = None

13

14class SignalGenerationLayer:

15 def __init__(self, confidence_threshold=0.30, min_signal_interval_bars=1):

16 self.confidence_threshold = confidence_threshold

17 self.min_signal_interval_bars = min_signal_interval_bars

18 self.last_signal_bar = -999

19

20 def generate_signal(self, inference_result: dict, current_bar: int,

21 current_time: datetime, model_name: str = 'primary') -> Optional[TradingSignal]:

22 confidence = inference_result['confidence']

23 prob_up = inference_result['probability_up']

24

25 if confidence < self.confidence_threshold:

26 return None

27 if (current_bar - self.last_signal_bar) < self.min_signal_interval_bars:

28 return None

29

30 direction = 'long' if prob_up > 0.5 else 'short'

31 self.last_signal_bar = current_bar

32 return TradingSignal(timestamp=current_time, direction=direction,

33 confidence=confidence, probability_up=prob_up, source_model=model_name)A confidence threshold of 0.30 on the normalized scale corresponds to raw probability above approximately 0.65 for long signals. Higher thresholds produce fewer but higher-quality signals; lower thresholds produce more signals with lower average quality.

Layer 5: Risk Management — The System That Keeps You in the Game

The risk management layer sits between signal and exchange. It receives a signal and returns a sized, risk-adjusted order — or no order at all if limits prevent trading.

Position Sizing with the Kelly Criterion

Where is the fraction of capital to risk, is win probability (from model output), is loss probability, and is the net odds ratio (average win / average loss). A fractional Kelly of 0.25–0.5 is used in practice to reduce variance.

1class RiskManagementLayer:

2 def __init__(self, portfolio_value: float, max_position_pct: float = 0.10,

3 max_drawdown_halt: float = 0.15, kelly_fraction: float = 0.25):

4 self.portfolio_value = portfolio_value

5 self.max_position_pct = max_position_pct

6 self.max_drawdown_halt = max_drawdown_halt

7 self.kelly_fraction = kelly_fraction

8 self.peak_value = portfolio_value

9 self.current_drawdown = 0.0

10

11 def update_portfolio_value(self, new_value: float):

12 self.portfolio_value = new_value

13 self.peak_value = max(self.peak_value, new_value)

14 self.current_drawdown = (self.peak_value - new_value) / self.peak_value

15

16 def compute_kelly_size(self, prob_up: float, avg_win: float, avg_loss: float) -> float:

17 p, q = prob_up, 1 - prob_up

18 b = avg_win / avg_loss if avg_loss > 0 else 1.0

19 kelly_full = max(0.0, (p * b - q) / b)

20 return kelly_full * self.kelly_fraction

21

22 def size_order(self, signal: TradingSignal, current_price: float,

23 avg_win: float = 0.02, avg_loss: float = 0.015) -> Optional[dict]:

24 if self.current_drawdown >= self.max_drawdown_halt:

25 print(f"RISK HALT: Drawdown {100*self.current_drawdown:.1f}% exceeds threshold")

26 return None

27

28 kelly_pct = self.compute_kelly_size(signal.probability_up, avg_win, avg_loss)

29 position_pct = min(kelly_pct, self.max_position_pct)

30 position_dollars = self.portfolio_value * position_pct

31 units = position_dollars / current_price

32

33 return {'direction': signal.direction, 'units': round(units, 6),

34 'position_dollars': round(position_dollars, 2),

35 'position_pct': round(position_pct, 4), 'current_drawdown': round(self.current_drawdown, 4)}The current drawdown: . When this reaches the halt threshold, the layer returns None — no order is sent. This mechanical circuit breaker prevents the most common path to catastrophic loss.

Layer 6: Order Execution — Where Decisions Become Trades

1class OrderExecutionLayer:

2 def __init__(self, exchange_id='binance', api_key='', api_secret='', paper_trading=True):

3 self.paper_trading = paper_trading

4 self.execution_log = []

5 if not paper_trading:

6 self.exchange = getattr(ccxt, exchange_id)({'apiKey': api_key, 'secret': api_secret, 'enableRateLimit': True})

7

8 def execute_order(self, order: dict, symbol: str, max_retries: int = 3) -> dict:

9 if self.paper_trading:

10 result = self._simulate_fill(order, symbol)

11 self._log_execution(order, result, 'paper')

12 return result

13

14 for attempt in range(max_retries):

15 try:

16 side = 'buy' if order['direction'] == 'long' else 'sell'

17 response = self.exchange.create_market_order(symbol, side, order['units'])

18 result = {'status': 'filled', 'order_id': response['id'],

19 'filled_price': response.get('average', None),

20 'filled_units': response.get('filled', order['units'])}

21 self._log_execution(order, result, 'live')

22 return result

23 except ccxt.NetworkError as e:

24 logging.warning(f"Network error on attempt {attempt+1}: {e}")

25 time.sleep(2 ** attempt)

26 except ccxt.ExchangeError as e:

27 logging.error(f"Exchange error: {e}")

28 result = {'status': 'rejected', 'reason': str(e)}

29 self._log_execution(order, result, 'live')

30 return result

31

32 return {'status': 'failed', 'reason': 'Max retries exceeded'}

33

34 def _simulate_fill(self, order: dict, symbol: str) -> dict:

35 slippage_bps = 5

36 factor = 1 + (slippage_bps / 10000) if order['direction'] == 'long' else 1 - (slippage_bps / 10000)

37 return {'status': 'paper_filled', 'simulated_price': round(order.get('current_price', 0) * factor, 2),

38 'filled_units': order['units']}Layer 7: Monitoring and Retraining — The System That Keeps the System Honest

1class MonitoringLayer:

2 def __init__(self, auc_window=30, auc_degradation_threshold=0.50, psi_retrain_threshold=0.25):

3 self.auc_window = auc_window

4 self.auc_degradation_threshold = auc_degradation_threshold

5 self.prediction_log = []

6

7 def log_prediction(self, timestamp, prob_up: float, actual_outcome: int):

8 self.prediction_log.append({'timestamp': timestamp, 'prob_up': prob_up, 'actual': actual_outcome})

9

10 def rolling_auc(self) -> float:

11 if len(self.prediction_log) < self.auc_window:

12 return None

13 recent = self.prediction_log[-self.auc_window:]

14 probs = [r['prob_up'] for r in recent]

15 actuals = [r['actual'] for r in recent]

16 if len(set(actuals)) < 2:

17 return None

18 return roc_auc_score(actuals, probs)

19

20 def check_health(self) -> dict:

21 auc = self.rolling_auc()

22 needs_retrain = False

23 alerts = []

24

25 if auc is not None:

26 if auc < self.auc_degradation_threshold:

27 alerts.append(f"CRITICAL: Rolling AUC {auc:.4f} below random baseline. Consider halting.")

28 needs_retrain = True

29 elif auc < self.auc_degradation_threshold + 0.03:

30 alerts.append(f"WARNING: Rolling AUC {auc:.4f} approaching degradation threshold.")

31

32 return {'rolling_auc': auc, 'n_predictions': len(self.prediction_log),

33 'needs_retrain': needs_retrain, 'alerts': alerts,

34 'status': 'HEALTHY' if not alerts else ('CRITICAL' if needs_retrain else 'WARNING')}When 30-day rolling AUC drops below 0.50 — the performance of a random classifier — the system is actively losing information. Continuing to trade on a model performing below random is strictly worse than not trading at all.

Key Takeaways

- A production AI trading system has seven distinct layers — each with defined inputs, outputs, and failure modes

- Feature engineering must use identical code in training, backtesting, and live inference — separate implementations guarantee silent degradation

- The model inference layer should be completely decoupled from trading logic — it receives features and returns probabilities, nothing more

- Kelly Criterion position sizing, capped at a maximum percentage and scaled fractionally, provides mathematically grounded sizing that adapts to model confidence

- The drawdown circuit breaker in the risk management layer is the most important single safety mechanism

- The monitoring layer is not optional — it is the mechanism by which the system remains honest about its own performance

Conclusion: Build the System, Not Just the Model

You now have the architectural blueprint for a system that can survive contact with live markets — not just a model that performs well in a notebook. The seven-layer architecture in this post is the structural pattern underlying production quantitative trading systems at every scale.

The next step is implementation. Start with Layer 1: download historical data, run it through validation logic, then build the feature engineering layer and confirm features are computed identically to how they will be in live inference. That single discipline eliminates one of the most common production failure modes before you have even trained a model.

Build upward through the layers. Test each independently before integrating. Paper trade the full pipeline for at least 30 days before committing live capital. Monitor rolling AUC from day one.

The architecture is now yours. The implementation is the work that separates those who trade well from those who trade at all.