AI Prediction Errors in Trading Systems

Discover the real causes of AI prediction errors in trading systems — overfitting, data leakage, regime shifts, and calibration errors. Learn diagnostic tools including learning curves, temporal permutation tests, rolling AUC monitoring, and PSI computation with full Python implementation.

Introduction: The Model That Destroyed a Fund

In 2007, a quantitative hedge fund running sophisticated statistical arbitrage strategies experienced what became known as the "Quant Quake" — a period of several days in August where dozens of well-backtested, heavily optimized models simultaneously collapsed, generating catastrophic losses across the industry. The models had not been hacked. The data feeds had not failed. The mathematics was not wrong.

The models had simply encountered something their training data could not have prepared them for: a correlated unwinding of positions across the entire quant industry that created market conditions statistically unlike anything in the historical record. Every prediction they made was wrong. Not occasionally — systematically wrong, at the worst possible moment.

Here is the counterintuitive truth that every AI-driven algo trader needs to internalize early: the danger of an AI prediction error is not just that it costs you money on a single trade. It is that AI models fail coherently — they make the same kind of wrong prediction repeatedly, in the same market conditions, in ways that compound losses rather than randomly distribute them.

Understanding exactly how and why AI prediction errors occur in trading systems is not a defensive skill. It is the skill that separates traders who survive long enough to compound from those who blow up on their first regime change.

In this post, you will learn the taxonomy of AI prediction errors — from the obvious to the deeply subtle — the mathematical diagnostics that reveal them before they destroy live capital, and the practical Python tools to detect, monitor, and mitigate each error type in a working trading system.

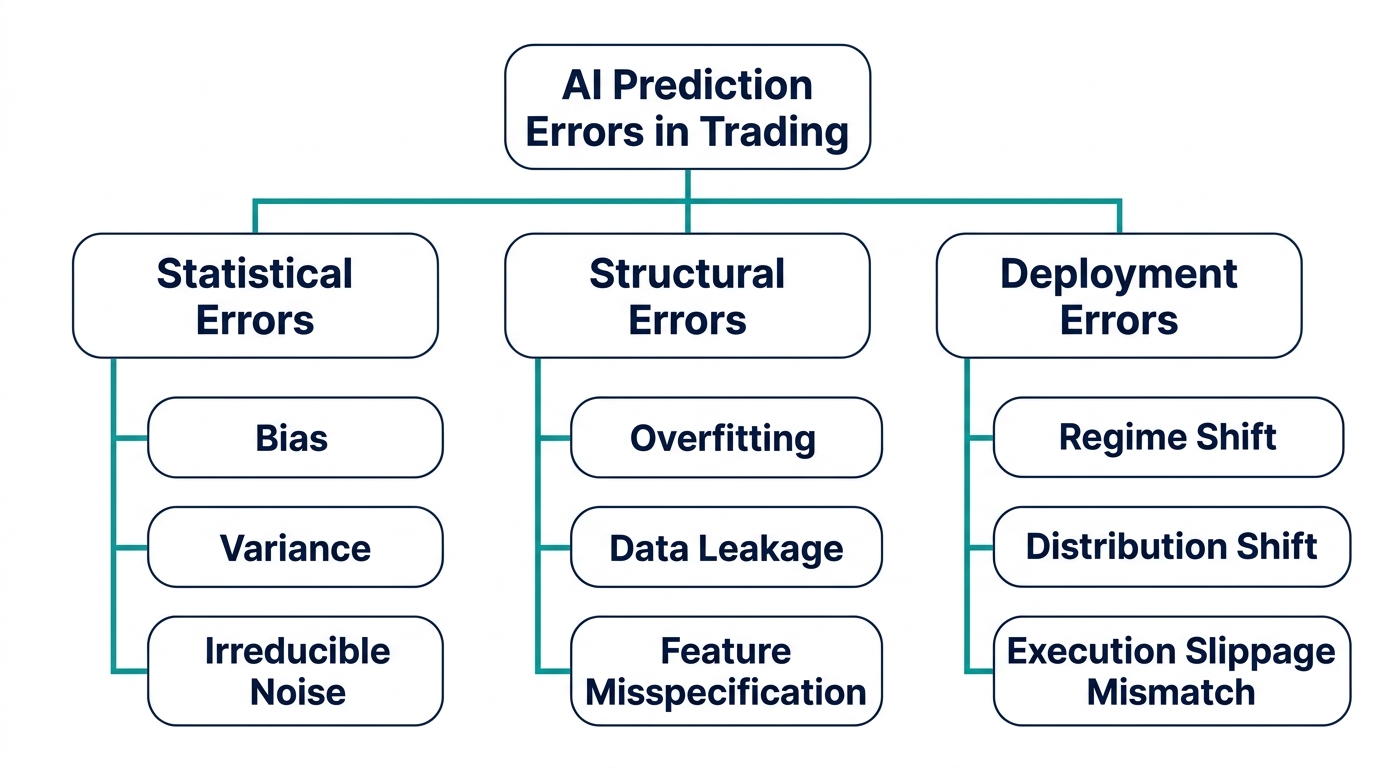

The Taxonomy of AI Prediction Errors in Trading

Not all prediction errors are created equal. Some are statistical. Some are structural. Some are invisible in backtesting but catastrophic in live deployment. The first step toward managing prediction errors is knowing which type you are dealing with — because the diagnosis determines the remedy.

Statistical Errors: Bias, Variance, and Noise

Every prediction error can be decomposed into three fundamental components. For a model making prediction of a true value :

Bias is the systematic error introduced by the model's assumptions. A model that assumes linear relationships in a nonlinear market will consistently predict in the wrong direction — not randomly, but predictably. High bias is the signature of underfitting.

Variance is the model's sensitivity to fluctuations in the training data. A high-variance model changes its predictions dramatically when trained on slightly different data samples — it has learned the noise rather than the signal. High variance is the signature of overfitting.

Irreducible noise () is the portion of prediction error that no model can eliminate, reflecting genuine randomness. In financial markets, this component is substantial. Any model appearing to predict with near-zero error on historical data has almost certainly memorized noise rather than learned signal.

The practical implication: you are always navigating a tradeoff. Reducing bias by adding complexity increases variance. The goal is not to minimize one or the other, but to find the complexity level at which total out-of-sample error is minimized.

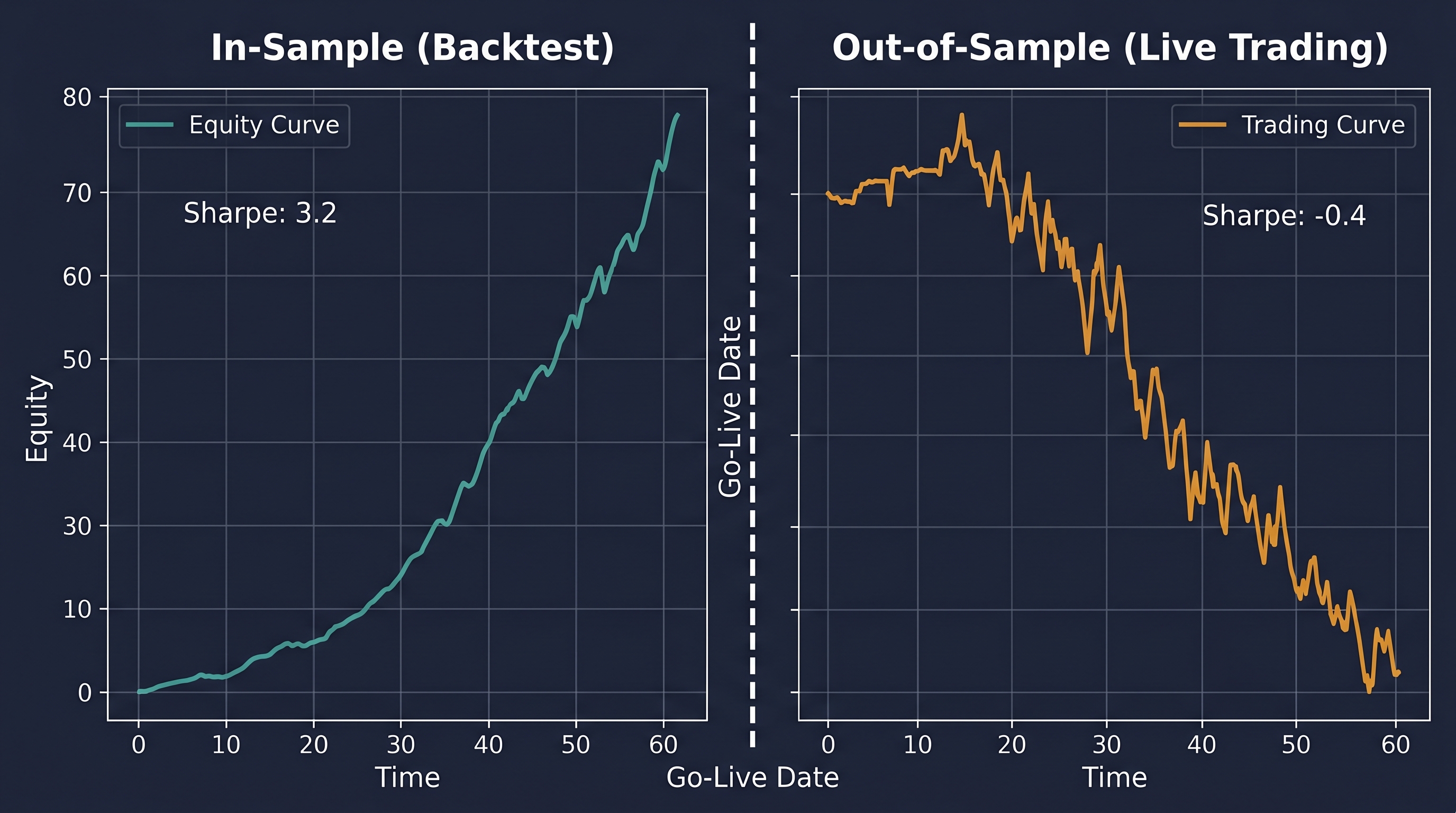

Overfitting: The Error That Looks Like Success

Overfitting is the most common and most dangerous AI prediction error in trading systems, precisely because it is invisible in backtesting. A model that has overfit produces a backtest that looks exceptional — high Sharpe, low drawdown, consistent returns. And then it fails completely in live trading.

The mechanism: a sufficiently complex model trained on historical data will eventually memorize every idiosyncratic fluctuation — random noise events, one-off reactions to specific news, microstructure artifacts. It mistakes these for repeatable patterns. When those exact conditions never recur in live markets, the model's predictions are worse than random on precisely the scenarios where it is most confident.

Diagnosing Overfitting with Learning Curves

1import numpy as np

2from sklearn.ensemble import RandomForestClassifier

3from sklearn.model_selection import learning_curve

4

5train_sizes, train_scores, val_scores = learning_curve(

6 estimator=RandomForestClassifier(n_estimators=200, max_depth=5, random_state=42),

7 X=X, y=y,

8 train_sizes=np.linspace(0.1, 1.0, 10),

9 cv=5, scoring='roc_auc', n_jobs=-1

10)

11

12train_mean = train_scores.mean(axis=1)

13val_mean = val_scores.mean(axis=1)The gap between training AUC and validation AUC is your overfitting signal. The generalization gap:

A gap above 0.10 in financial models warrants immediate investigation. Above 0.20 means the model should not be deployed. The remedy is regularization: reducing model depth, adding dropout or L2 weight penalties, or reducing feature count.

Data Leakage: The Invisible Contamination

If overfitting is the most common error, data leakage is the most insidious — producing the most convincing false signals with no obvious explanation for the live trading gap.

Target Leakage

Target leakage happens when features contain information about the target variable that would not be available at prediction time. For every feature, explicitly trace which rows of historical data it uses. If any overlap with or postdate the target being predicted, you have leakage.

1# WRONG: Computes rolling mean on full dataset before split

2df['rolling_mean'] = df['close'].rolling(20).mean()

3X = df[['rolling_mean', 'rsi']].values

4X_train, X_test = X[:split], X[split:] # Leakage already baked in

5

6# CORRECT: Ensure all features computable from data available at prediction time

7df['rolling_mean'] = df['close'].rolling(20).mean()

8df['target'] = df['close'].shift(-1) > df['close']

9df.dropna(inplace=True)Train-Test Contamination

1# WRONG: Scaler fitted on full dataset leaks test statistics into training

2scaler = StandardScaler()

3X_scaled = scaler.fit_transform(X)

4

5# CORRECT: Scaler fitted only on training data

6scaler = StandardScaler()

7X_train = scaler.fit_transform(X[:split])

8X_test = scaler.transform(X[split:])The Leakage Detection Test

1import numpy as np

2from sklearn.metrics import roc_auc_score

3

4model.fit(X_train, y_train)

5true_auc = roc_auc_score(y_test, model.predict_proba(X_test)[:, 1])

6

7y_train_shuffled = np.random.permutation(y_train)

8model.fit(X_train, y_train_shuffled)

9shuffled_auc = roc_auc_score(y_test, model.predict_proba(X_test)[:, 1])

10

11print(f"True AUC: {true_auc:.4f}")

12print(f"Shuffled Target AUC: {shuffled_auc:.4f}")If shuffling training labels does not significantly reduce test AUC, your model is not learning a genuine temporal relationship — it is exploiting structural features of the data arrangement, a strong indicator of leakage. A practical heuristic: if your model achieves validation AUC above 0.65 on daily price prediction without exotic data sources, be suspicious. Genuinely predictive signals rarely exceed 0.58–0.62 on properly held-out data.

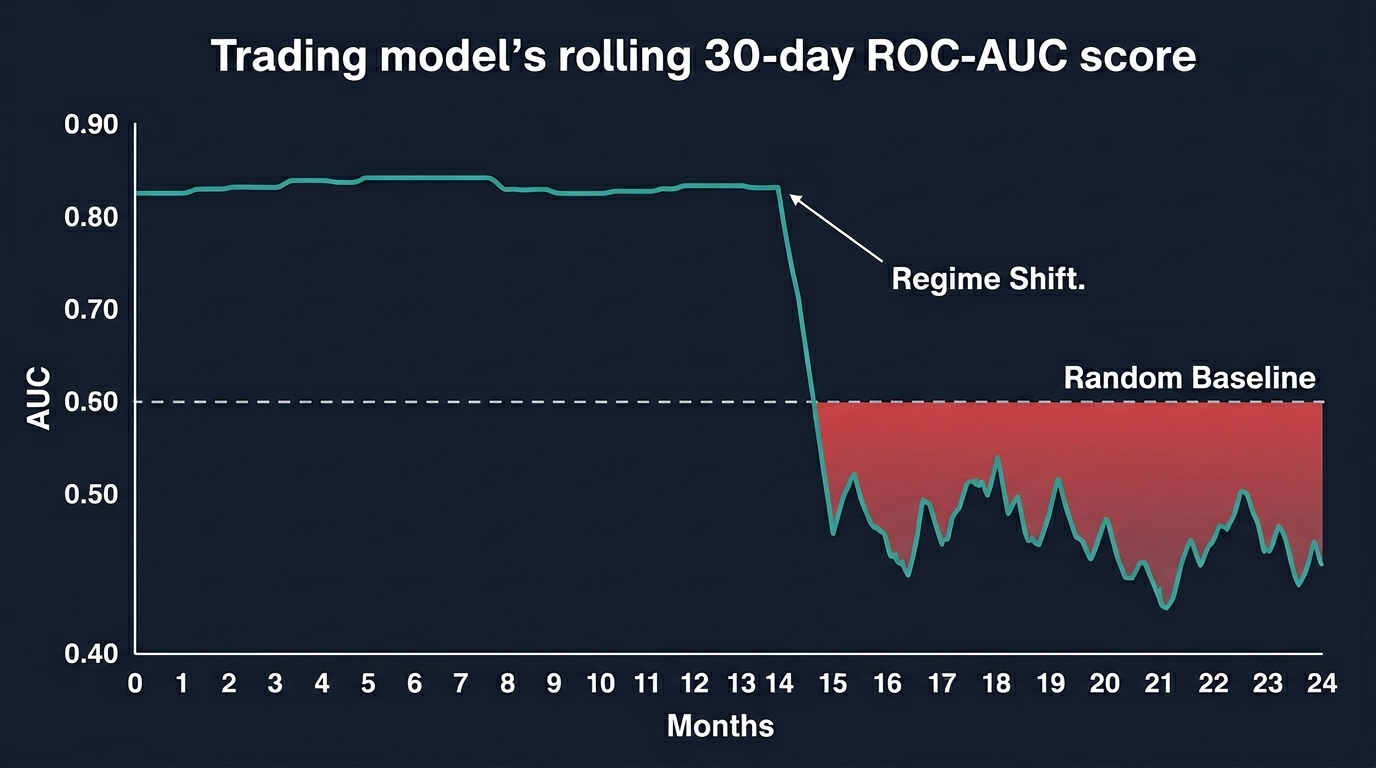

Regime Shift Errors: When the World Changes

Even a perfectly specified, properly trained, leakage-free model will eventually fail — because financial markets are non-stationary. The statistical relationships that held during training degrade, reverse, or disappear as market regimes change.

Monitoring for Regime-Induced Prediction Degradation

1def rolling_model_performance(y_true, y_prob, window=30):

2 """Compute rolling ROC-AUC to detect regime-driven degradation."""

3 results = []

4 for i in range(window, len(y_true)):

5 window_true = y_true[i - window:i]

6 window_prob = y_prob[i - window:i]

7 if len(np.unique(window_true)) < 2:

8 results.append(np.nan)

9 continue

10 auc = roc_auc_score(window_true, window_prob)

11 results.append(auc)

12 return pd.Series(results, name='rolling_auc')

13

14rolling_auc = rolling_model_performance(y_actual_live, y_prob_live, window=30)

15DEGRADATION_THRESHOLD = 0.50

16if rolling_auc.iloc[-1] < DEGRADATION_THRESHOLD:

17 print("ALERT: Model performance degraded below random baseline.")When 30-day rolling AUC falls below 0.50, the model has entered a regime where its learned patterns are actively counterproductive. Continuing to trade is worse than flipping a coin.

The Population Stability Index: Detecting Distribution Shift

Where is the proportion of training samples in bin , and is the corresponding proportion in live data. PSI below 0.10 = stable. 0.10–0.25 = monitor. Above 0.25 = significant shift — retrain.

1def compute_psi(train_feature, live_feature, n_bins=10):

2 """Compute PSI between training and live feature distributions."""

3 breakpoints = np.percentile(train_feature, np.linspace(0, 100, n_bins + 1))

4 breakpoints[0], breakpoints[-1] = -np.inf, np.inf

5

6 train_counts = np.histogram(train_feature, bins=breakpoints)[0]

7 live_counts = np.histogram(live_feature, bins=breakpoints)[0]

8 train_pct = (train_counts + 0.0001) / len(train_feature)

9 live_pct = (live_counts + 0.0001) / len(live_feature)

10

11 psi = np.sum((live_pct - train_pct) * np.log(live_pct / train_pct))

12 return psi

13

14for feature in ['rsi', 'volatility', 'vol_zscore', 'lag_1', 'lag_3']:

15 psi = compute_psi(X_train_df[feature].values, X_live_df[feature].values)

16 status = "STABLE" if psi < 0.10 else "MONITOR" if psi < 0.25 else "RETRAIN"

17 print(f"{feature}: PSI = {psi:.4f} — {status}")Calibration Errors: When Probabilities Lie

A well-calibrated model that outputs 70% probability should be right ~70% of the time. A poorly calibrated model might output 70% confidence on predictions actually right only 52% of the time — leading to dramatically over-sized positions based on false confidence.

The Expected Calibration Error (ECE):

Where is the number of probability bins, is predictions in bin , is actual accuracy, and is mean predicted confidence. A perfectly calibrated model has ECE of 0.

1from sklearn.calibration import calibration_curve, CalibratedClassifierCV

2

3fraction_of_positives, mean_predicted_value = calibration_curve(

4 y_test, y_prob, n_bins=10

5)

6

7# Apply Platt scaling to recalibrate

8calibrated_model = CalibratedClassifierCV(base_model, cv='prefit', method='sigmoid')

9calibrated_model.fit(X_val, y_val)

10y_prob_calibrated = calibrated_model.predict_proba(X_test)[:, 1]Platt scaling fits a logistic regression layer on top of raw model outputs, adjusting predicted probabilities to match observed frequencies. After calibration, a 70% prediction corresponds more reliably to a 70% empirical win rate.

Key Takeaways

- AI prediction errors fail coherently, not randomly — they compound losses, making error type identification a critical risk management skill

- The bias-variance-noise decomposition provides the foundational diagnostic framework for understanding error sources

- Overfitting produces backtests that look exceptional and live strategies that fail immediately — learning curves and AUC gaps are the diagnostic tools

- Data leakage through target or train-test contamination produces artificially inflated backtests — the temporal permutation test is the practical detection heuristic

- Regime shift errors are environmental, not model failures — rolling AUC monitoring and PSI computation are essential circuit breakers

- Calibration errors cause position sizing to be systematically misleading — Platt scaling corrects miscalibration without retraining the model

- Every prediction error has a readable signature — build the diagnostic infrastructure before you need it

Conclusion: Error Awareness Is the Real Alpha

The traders who generate durable returns from AI trading systems are not necessarily those who build the most sophisticated models. They are the ones who understand their models' failure modes with clinical precision, who have built monitoring infrastructure that detects degradation before it becomes catastrophic, and who treat every unexpected loss not as bad luck but as diagnostic data.

Every prediction error has a signature. Overfitting shows in the generalization gap. Data leakage shows in implausibly high backtest performance. Regime shift shows in declining rolling AUC. Calibration error shows in the reliability diagram. These signatures are readable before you have lost significant capital — but only if you have built the diagnostic infrastructure to read them.

The code in this post runs on any dataset where you have model predictions and corresponding outcomes. Start by running the learning curve diagnostic on your current model. Then run the leakage detection test. Then build the rolling AUC monitor as a live dashboard metric. Each tool reveals something the raw equity curve cannot.

The market will eventually find every weakness in your system. The question is whether you find those weaknesses first, on paper, in a controlled diagnostic environment — or whether the market finds them for you, in live capital, at the worst possible moment.

Build the diagnostics. Run them before every deployment. Treat error analysis not as a post-mortem exercise but as an ongoing discipline. That discipline — more than any single model improvement — is what separates systems that survive from systems that do not.